Ocean Mortgage 2020 Newsletter 011 |

|

|

|

|

|

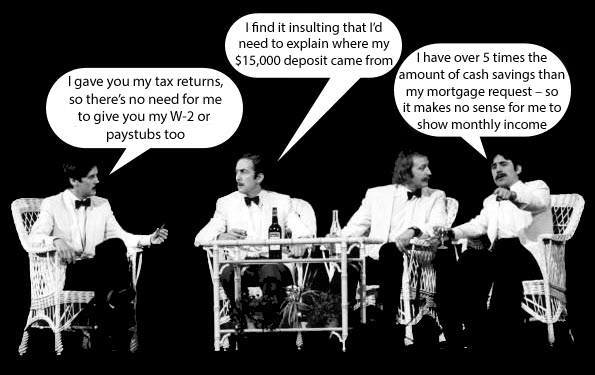

MORTGAGE DEAL BREAKERS |

There is nothing wrong with the above statements, but unfortunately the bad apple borrowers have spoiled it for new borrowers. It is completely understandable that consumers would think twice about having to “jump through hoops” just to get a mortgage – especially in situations where they have stellar credit, lots of liquidity, and consistent earnings.

But lenders and regulators needed to stop the games being played:

- Borrowers fabricating tax return figures to show inflated income

- Borrowers selling contraband and laundering illegally obtained funds

- Borrowers getting funds from friends and family that were really loans, not gifts

It really does make sense that all borrowers should be required to show they have an “ability to repay” their mortgage. Fannie Mae, Freddie Mac and FHA do not give special treatment to anyone – and therefore no one is viewed as being more entitled than anyone else.

Just because someone has significant cash or retirement savings doesn’t mean they won’t use it for some other purpose right after the loan closes – i.e., to buy a business, a large boat or some other investment. Such a purchase could leave next to nothing for mortgage payments. Therefore, even someone with a large 401k or IRA needs to establish a monthly income distribution to satisfy a lender.

It could be more economical to borrow money instead of selling investments that have adverse tax consequences. But it would be far less costly, less time-consuming and less frustrating to instead arrange a margin loan collateralized by an investment portfolio. |

|

|

|

NMLS #901949 (Company)

NMLS #880882 (Individual) |

|

|

|

|

|